If you run a business in Kenya and process payroll manually — or worse, with a generic spreadsheet template — you are exposed to real compliance risk every single month. Kenya has four distinct statutory deduction obligations, administered by three separate government bodies, with contribution rules and tax bands that have changed significantly in the 2024/2025 fiscal year.

Getting one deduction wrong — an incorrect PAYE band, a missing Housing Levy calculation, an NSSF contribution that doesn't reflect the current rate — can trigger KRA penalties, employee disputes, and audit exposure. And yet most Kenyan SMBs are still running payroll from a spreadsheet built by someone who left the company years ago.

This article explains exactly how Kenyan payroll compliance works, why it is genuinely complex, and how HRMS Kenya automates every mandatory deduction so your payroll is right every month — without a calculator in sight.

Who this is for: HR managers, Finance officers, and business owners at Kenyan companies — and East African businesses with staff in Kenya — who want to understand and automate their statutory payroll obligations.

Why Kenyan Payroll Compliance Is Uniquely Complex

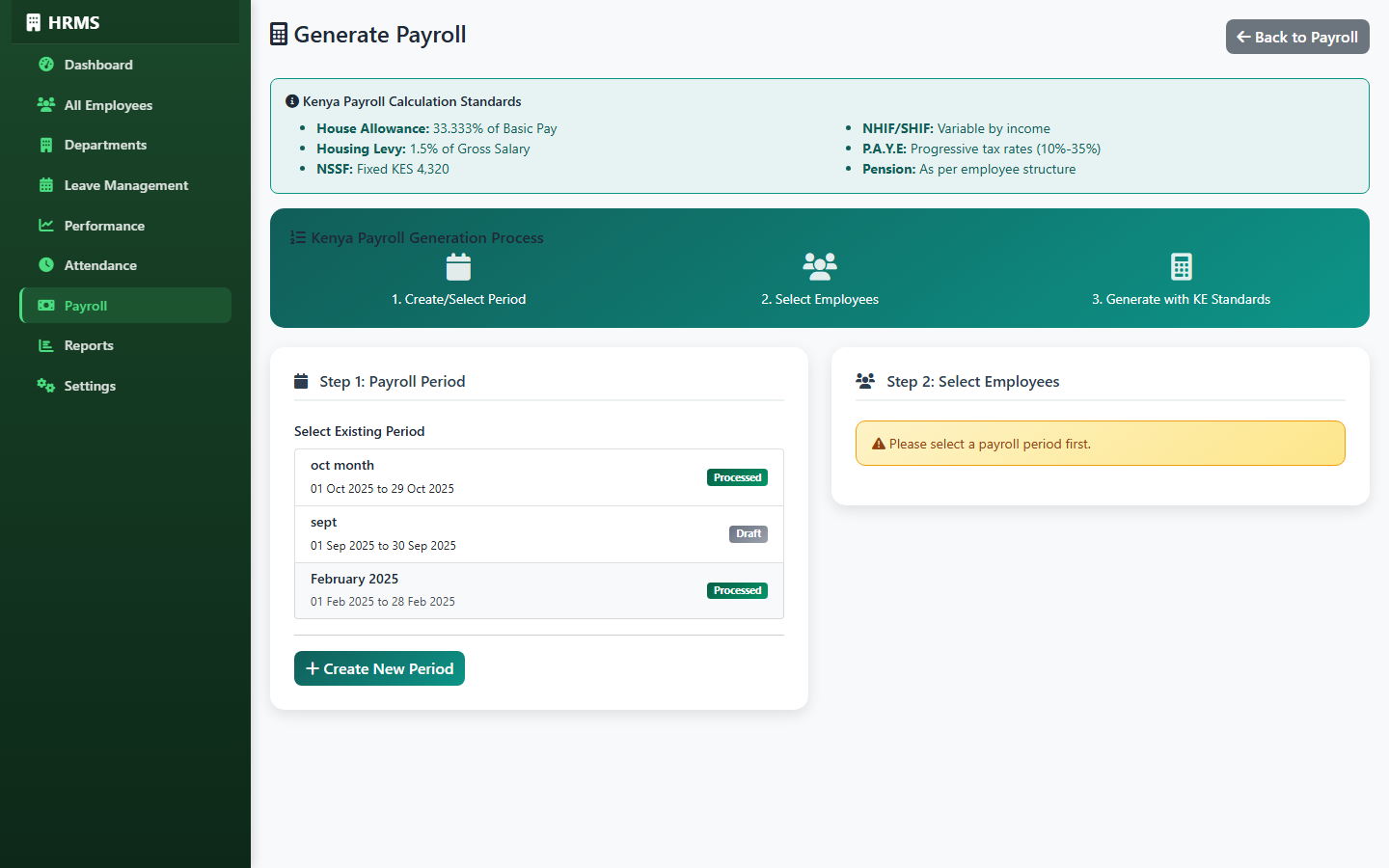

Payroll in many countries involves one or two statutory deductions administered by a single body. Kenya has four mandatory deductions, administered by three separate government agencies — KRA, NHIF/SHIF, and NSSF — plus the Housing Fund under the Affordable Housing Levy Act. Each has its own rates, remittance deadlines, and penalty structures for non-compliance.

Compounding this, the 2024/2025 period brought significant changes. The NSSF Act 2013 contribution tiers were clarified and are now actively enforced at KES 4,320 per month. The Affordable Housing Levy, introduced in 2023 and confirmed by the Finance Act 2023, is now fully operational at 1.5% of gross salary. NHIF is in an active transition to SHIF (Social Health Insurance Fund) under the Social Health Insurance Act 2023, with contribution structures in flux.

For a small business running payroll manually, keeping up with these changes — and applying them correctly to every employee's calculation — is a significant and ongoing burden. For a business that hasn't updated its payroll spreadsheet in 18 months, it's a ticking compliance clock.

Remittance deadline: All statutory deductions — PAYE, NHIF/SHIF, NSSF, and Housing Levy — must be remitted to the respective bodies by the 9th of the following month. Missing this deadline triggers penalties and interest on the outstanding amount.

The Four Mandatory Deductions Every Kenyan Employer Must Handle

1. PAYE — Pay As You Earn Income Tax (KRA)

PAYE is administered by the Kenya Revenue Authority and is deducted at source by the employer. It applies to all employment income: basic salary, allowances, benefits in kind, and bonuses. The calculation uses a graduated tax band structure under the 2024/2025 KRA rates.

The current PAYE bands are as follows:

| Monthly Taxable Income (KES) | Tax Rate | Max Tax in Band (KES) |

|---|---|---|

| 0 – 24,000 | 10% | 2,400 |

| 24,001 – 32,333 | 25% | 2,083 |

| Above 32,333 | 30% | On the balance |

Once the gross tax is calculated from the bands, Personal Relief of KES 2,400 per month is subtracted automatically to arrive at the net PAYE payable. This relief applies to all resident employees regardless of income level. Insurance Relief and mortgage interest relief may also apply where applicable.

Taxable income is gross pay minus allowable deductions — including the NSSF employee contribution. This means that calculating PAYE correctly requires knowing the NSSF deduction first, making the order of calculation critical.

2. NHIF / SHIF — National Health Insurance Fund

NHIF contributions fund employee access to medical cover under the national scheme. Kenya is transitioning from NHIF to SHIF (Social Health Insurance Fund) under the Social Health Insurance Act 2023. Under the new SHIF framework, contributions are calculated as a percentage of gross salary rather than the previous tiered flat rate structure.

Both employer and employee are required to contribute. HRMS Kenya applies the current contribution rates as published and is updated to reflect changes as they come into effect. The contribution is remitted to NHIF/SHIF by the 9th of the following month, separately from PAYE and NSSF.

3. NSSF — National Social Security Fund

Under the NSSF Act 2013 as currently enforced, the monthly employee NSSF contribution is KES 4,320 — a fixed amount, with a matching employer contribution of KES 4,320. This is a significant change from the pre-2013 Act regime where contributions were capped at much lower levels. The Act was confirmed as enforceable following court processes and is now the active standard for Kenyan employers.

NSSF contributions are deducted from gross pay before PAYE is calculated, since they are an allowable deduction against taxable income. This sequence matters and must be handled correctly in your payroll calculation.

4. Affordable Housing Levy

The Affordable Housing Levy was introduced under the Affordable Housing Act and the Finance Act 2023. Both employee and employer contribute 1.5% of the employee's gross salary each. This is calculated on the full gross pay — before any other deductions — and remitted to the Housing Fund separately from other statutory obligations.

Common error: Some employers apply the Housing Levy only to the employee and omit the employer portion, or calculate it on net rather than gross pay. Both are non-compliant. The levy applies to both parties at 1.5% each on gross salary.

The Risk of Getting It Wrong

Kenyan statutory compliance penalties are not theoretical. The KRA has significantly increased audit activity and can assess unpaid PAYE with interest and penalties retrospectively for up to seven years. NSSF and NHIF non-remittance also attracts penalties and can result in directors being held personally liable in cases of persistent default.

Beyond regulatory penalties, payroll errors damage employee trust. If an employee receives a payslip with an incorrect deduction — whether too high or too low — it creates an immediate HR problem. Too-low deductions today mean either a correcting deduction (which feels like a pay cut) or an employer absorbing the shortfall. Neither outcome is good.

The Audit Exposure Problem

A payroll spreadsheet that was "built by someone in the finance team" often has no audit trail. If KRA asks for three years of payroll records to verify PAYE compliance, can you produce them? In HRMS Kenya, every payroll run is stored, timestamped, and reportable. The statutory reports you need for a KRA audit are generated in seconds, not reconstructed from old spreadsheets.

The Scaling Problem

Manual payroll that works for 10 employees becomes error-prone at 25 and unmanageable at 50. The number of calculations compounds with headcount. HRMS Kenya applies the same calculation logic to every employee on every run — consistently, without the fatigue and distraction that affects manual calculation.

Example calculation: An employee earning KES 80,000 gross per month. NSSF: KES 4,320 (fixed). Housing Levy employee portion: KES 1,200 (1.5% of 80,000). Taxable income for PAYE: KES 80,000 − KES 4,320 = KES 75,680. PAYE gross tax: KES 2,400 (on first 24,000 at 10%) + KES 2,083 (on next 8,333 at 25%) + KES 13,004 (on remaining 43,347 at 30%) = KES 17,487. Less Personal Relief KES 2,400 = Net PAYE: KES 15,087. Net pay: KES 80,000 − KES 4,320 − KES 1,200 − KES 15,087 − NHIF/SHIF = final take-home. HRMS Kenya calculates all of this automatically for every employee on your payroll.

What HRMS Kenya Does Beyond Payroll

Payroll compliance is the most critical module, but HRMS Kenya is a full HR management platform. Kenyan businesses need more than a payroll calculator — they need a system that handles the complete employee lifecycle, from hire to payslip and beyond.

Employee Self-Service: What It Means for Your HR Team's Workload

One of the highest-friction areas in any HR function is the constant stream of employee enquiries: "Can I see my payslip?", "How many leave days do I have left?", "What are my PAYE deductions this month?" Each of these questions requires your HR team to look something up and respond — a trivial task individually, but a significant time drain across a team of 30 or 50 people.

HRMS Kenya's Employee Self-Service portal gives each employee direct access to their own data:

- View and download payslips with full KES breakdown (gross pay, all statutory deductions, net pay)

- Apply for leave and track approval status in real time

- Check their own attendance calendar and monthly summary

- View active performance goals and historical review results

The payslip is particularly important from a compliance and employee relations perspective. An employee who can see their PAYE, NSSF, NHIF/SHIF, and Housing Levy deductions clearly labelled — with the gross and net pay transparently displayed — has no reason to question whether their employer is deducting correctly. Transparency builds trust and reduces the HR queries that come from confusion about the payslip.

From Hire to Payslip: The Full Employee Lifecycle in HRMS Kenya

Create the employee profile

Enter personal details, employment type, department, job title, salary, and statutory identifiers: KRA PIN, NSSF number, bank account for net pay transfer.

Attendance and leave tracking begins

The employee starts appearing in daily attendance registers. Leave entitlements accrue automatically based on your configured policy. Managers see the employee in team leave calendars from day one.

Performance cycle set up

Goals and KPIs are assigned. Review periods are scheduled. Line managers receive prompts when reviews are due — no chasing required.

Monthly payroll run

HRMS Kenya pulls attendance data, applies the employee's salary structure, and calculates all four statutory deductions automatically. Review the payroll summary, approve, and generate payslips.

Payslip distributed; reports generated

Each employee's payslip is available in their self-service portal immediately after payroll approval. Statutory reports for KRA, NSSF, NHIF/SHIF, and Housing Levy are generated and ready for remittance before the 9th.

How HRMS Kenya Compares to Spreadsheet-Based Payroll

❌ Spreadsheet Payroll

- PAYE bands manually updated (or not)

- NSSF rate may still reflect old KES 200 cap

- Housing Levy often missing entirely

- No audit trail for historical runs

- Payslips manually formatted per employee

- Statutory reports built from scratch each month

- One formula error affects all employees

- No employee self-service access

✓ HRMS Kenya

- PAYE calculated on KRA 2024/2025 bands

- NSSF fixed at KES 4,320 (both employee and employer)

- Housing Levy at 1.5% — both sides — auto-calculated

- Full audit trail with timestamps per run

- Payslips generated automatically for all employees

- Statutory reports generated in one click

- Consistent calculation logic for every employee

- Employee self-service portal for payslips and leave

Setting Up Payroll for Your First Kenyan Employee

Getting started with HRMS Kenya requires three things before you can run your first payroll: the employee profile, the salary structure, and the company statutory registration details.

What you need for each employee

- KRA PIN — required for PAYE deduction and iTax submissions

- NSSF membership number — for remittance matching

- NHIF/SHIF number — for health contribution allocation

- Bank account details — for net pay direct transfer

- Gross monthly salary — the basis for all deduction calculations

- Employment start date — determines leave accrual and probation status

Company-level setup

At the company level, you configure your KRA employer PIN, NSSF employer number, NHIF/SHIF employer code, and Housing Levy registration. These appear on all statutory reports and remittance schedules generated by the system.

Once both are in place, the first payroll run is largely automated. HRMS Kenya fetches the employee's attendance data for the month, applies the salary structure, runs the calculation sequence (NSSF → Housing Levy → PAYE → NHIF/SHIF), and produces both the payslip and the statutory remittance report. From setup to first payslip, most teams are operational within a day.

Automate Your Kenyan Payroll Compliance

Stop recalculating PAYE bands manually and hoping your Housing Levy formula is correct. HRMS Kenya handles every statutory deduction — every month — and gives every employee a clear, accurate payslip in KES.

Explore HRMS Kenya → Book a DemoFrequently Asked Questions

Bottom Line

Kenyan payroll compliance requires getting four separate statutory deductions right, every month, for every employee — and remitting each to a different body before the 9th. The rates have changed materially in the 2024/2025 period. The penalties for non-compliance are real and retrospective.

HRMS Kenya exists specifically to remove this burden from Kenyan HR and Finance teams. It calculates PAYE on the current KRA bands, applies NSSF at KES 4,320, deducts Housing Levy at 1.5% from both sides, handles NHIF/SHIF at current rates, applies Personal Relief of KES 2,400, and produces a clear payslip in KES — automatically, every payroll cycle.

If your current payroll process involves a spreadsheet, a calculator, and a prayer that the formula someone built is still correct — it's time to replace it with something that was built for this. HRMS Kenya is that system.